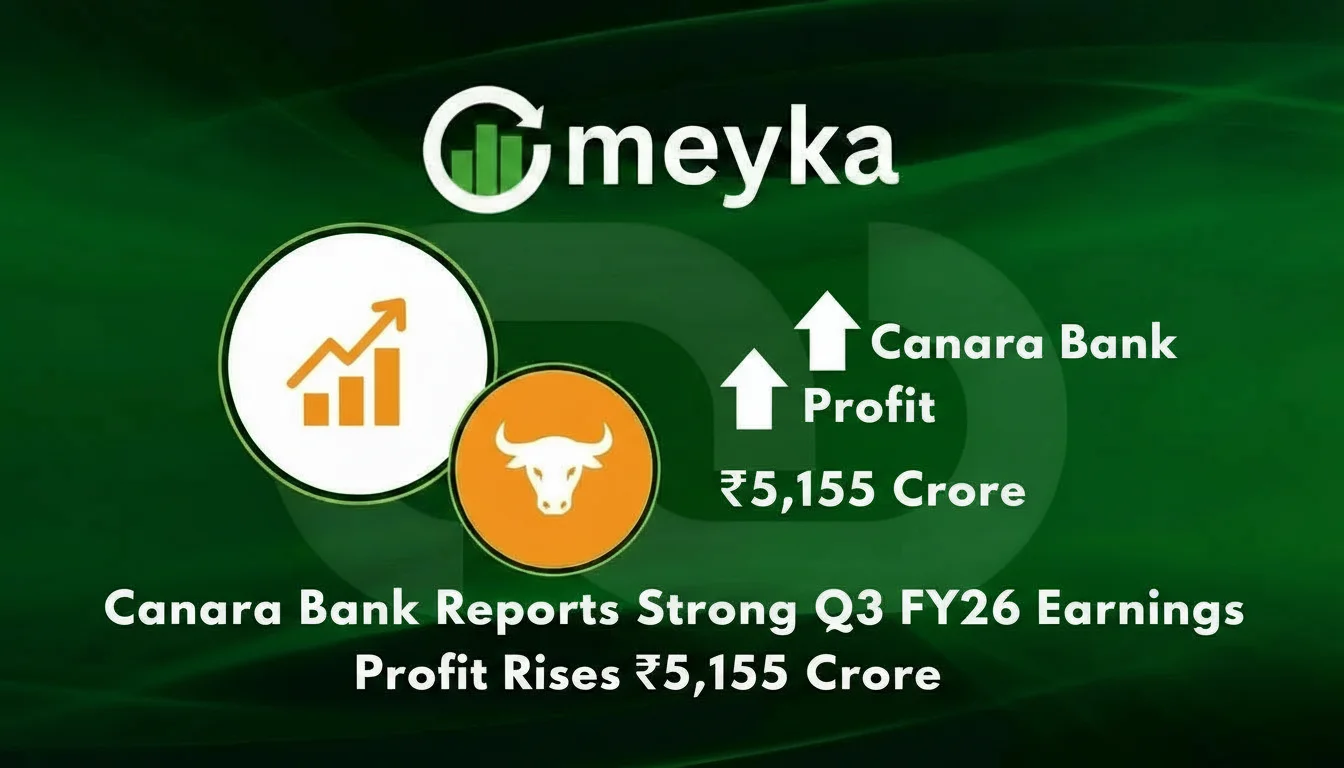

Canara Bank Reports Strong Q3 FY26 Earnings, Profit Rises ₹5,155 Crore

Canara Bank has delivered impressive financial results for the third quarter of the fiscal year 2025-26, reporting a significant rise in net profit and healthy business growth across its core banking operations. The strong performance reflects improving asset quality, robust credit demand in key segments, and disciplined cost management. This result reinforces Canara Bank’s position as one of India’s leading public sector banks in a competitive financial services landscape.

Continue Reading on Meyka

This article is available in full on our main platform. Get access to complete analysis, stock insights, and more.

Read Full Article →