The Bank of Canada has cut its key interest rate to 2.5%. This marks a big shift in policy after months of holding steady. It shows how the central bank is now more focused on growth than fighting inflation.

We know Canada has been dealing with slowing demand, high debt, and weaker job numbers. Inflation is cooling, but the economy is not moving at the same pace. This cut is meant to give households and businesses some relief. Lower borrowing costs can help families manage mortgages and give small firms room to invest.

But there is another side too. Rate cuts can boost housing demand, increase household debt, and create new risks if inflation rebounds. That’s why many people are watching this move closely.

As we examine this policy shift, we will explore why the Bank of Canada made this decision, how markets responded, and what it means for us in our daily lives. In the end, it’s not just about numbers. It’s about finding a balance between growth, prices, and stability.

Background and Recent Context

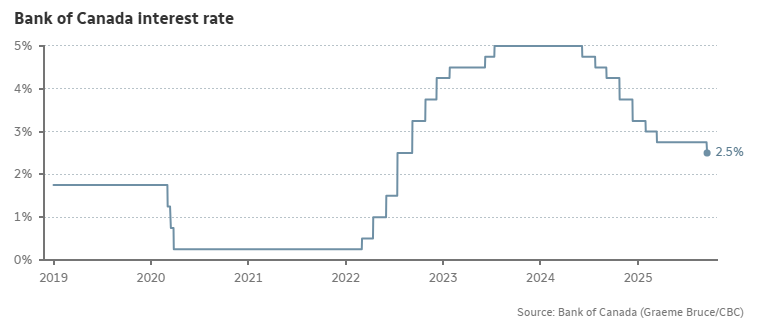

On September 17, 2025, the Bank of Canada cut its policy rate by 25 basis points to 2.5%. This is the first cut since March and the lowest level in about three years. The Bank set the Bank Rate at 2.75% and the deposit rate at 2.45%. Recent data showed the economy slipping. Q2 GDP fell, and the job market weakened. Unemployment rose in August.

Inflation has cooled from its peak. Core measures hover near the top of the target range. That gave the Bank room to act. Exports and business investment fell after higher U.S. tariffs. This weighed on growth. The Bank pointed to trade shocks as a major risk. The labour market lost strength. Recent months saw large job declines. Slower hiring reduced household income and spending. Taken together, the Bank judged that modest easing would better balance risks to growth and inflation. The message was cautious.

Immediate Market Reaction

The Globe & Mail Source: Canadian Dollar Price Overview

The Canadian dollar fell modestly after the announcement. Currency markets often react quickly to rate changes. Short-term bond yields moved lower as traders priced in easier policy. Equities rallied in some sectors, especially banks and real estate stocks. Markets also priced in a chance of more cuts before year-end. Some economists expect an additional quarter-point move if data weaken further.

Impact on Businesses

Lower interest rates cut borrowing costs for firms. That helps small businesses with loans and lines of credit. It also eases refinancing pressure for debt-heavy companies.

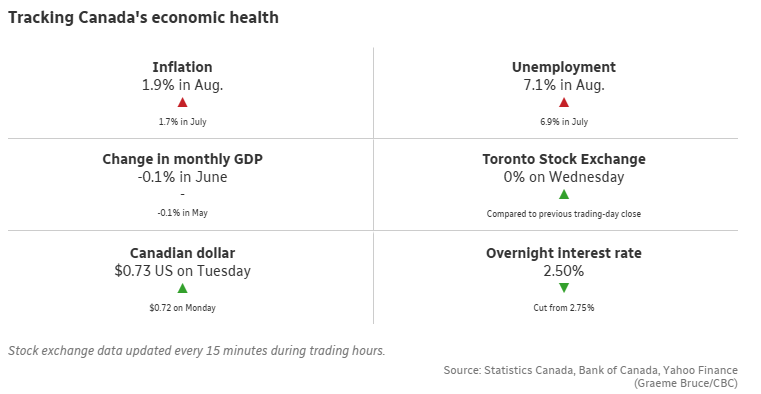

CBC Source: Canada’s Current Economic Conditions

Cheaper credit may encourage more capital spending. But firms facing weak demand or export slumps may still delay plans. The policy boost is not a cure-all. Export-dependent sectors remain vulnerable. If global demand stays weak, lower rates at home cannot fully offset lost sales abroad.

Impact on Consumers

Mortgage rates tend to fall after central bank cuts. That eases monthly payments for new and variable-rate borrowers. Lower rates can raise disposable income. That should support household spending. But rising unemployment may limit gains in demand. Cheaper credit also risks higher household borrowing. If lending rises too fast, debt profiles could worsen. Policymakers will watch credit growth closely.

Implications for the Housing Market

Lower mortgage costs usually lift housing demand. That can help buyers who struggled under higher rates. However, faster demand may push prices up again. That poses a policy trade-off: support the economy or curb housing risks. The Bank must weigh both.

Risks and Concerns

A main risk is reigniting inflation. If demand recovers too fast, price pressures could return. The Bank signalled caution on this point. Global shocks remain a threat. Tariffs, trade frictions, or a slowdown in major trading partners could force further action. External forces complicate domestic policy. Another risk is household debt. Lower rates can encourage more borrowing. High debt could amplify future shocks.

Expert Views and Forward Guidance

Tune in tomorrow for an exclusive interview with Tiff Macklem, Governor of the @bankofcanada, in a conversation with WONK host @AmandaLang about the bank’s rate cut decision, affordability, #tariffs and more.

Governor Tiff Macklem said the Bank is ready to cut further if risks rise. He emphasised careful monitoring of jobs, inflation, and trade. Many analysts see scope for another cut before year-end if the labour market keeps weakening. Others warn that the easing cycle may be shallow. Markets will watch the October 29 policy meeting for fresh guidance. That meeting could clarify the path ahead.

What to watch next?

Key indicators to track include monthly job reports, retail sales, and Q3 GDP. Any inflation surprise will also shape the outlook. Watch Canada’s trade data and U.S. policy moves closely. Cross-border trade policy and U.S. rate decisions can change Canada’s economic path quickly.

Bottom Line

The cut to 2.5% aims to ease pressure on growth and the job market. The move is cautious and data-driven. Lower rates will help borrowers and some firms. They also bring choices: encourage demand or guard against higher prices and more debt. Close monitoring of jobs, inflation, and trade will shape future steps.

Frequently Asked Questions (FAQs)

Did the Bank of Canada cut rates?

Yes. On September 17, 2025, the Bank of Canada cut its key policy interest rate from 2.75% to 2.50%.

Is the Bank of Canada going to cut rates in 2025?

Experts expect one more rate cut before the end of 2025. That cut may bring the policy rate down to about 2.25% if the economy weakens.

What happens when a bank cuts rates?

When a bank cuts rates, borrowing costs fall. Loans and mortgages become cheaper. That can boost spending. But inflation risk may rise.

Disclaimer:

The above information is based on current market data, which is subject to change, and does not constitute financial advice. Always do your research.