Bank Earnings to Close a Strong 2025 and Set the Stage for Growth in 2026

Bank earnings finished 2025 on a strong note, surprising many analysts and investors alike. Major banks like JPMorgan Chase and Bank of America are reporting solid profits as of January 2026, with healthy net interest income and steady fee growth.

This strength comes even as global economies face uncertainty. Low interest rates and rising loan demand helped lift bank revenues. At the same time, markets reacted positively to increased deal activity and better credit quality.

Investors are now looking ahead. The big question is whether this momentum will carry into 2026. Early signs point to cautious optimism. Banks are preparing to invest more in technology and expand lending, while keeping an eye on costs and risk.

Let’s explore those trends and what they mean for banks and the broader economy in the year ahead.

What Made 2025 a Strong Year for Banks?

In 2025, banks globally ended the year with solid earnings. Net interest income (NII) was a key driver. More loans and better deposit pricing pushed interest earnings higher. Many banks also grew their fee income from advisory work, trading, and wealth management. Investment banking deals, often worth billions, helped revenue beyond core lending.

Analysts saw strong credit quality overall, with banks building better buffers against loan losses, an important sign of strength as 2026 approaches. U.S. banks like JPMorgan Chase, Bank of America, and others delivered profits that beat market expectations late in 2025, lifting confidence in the sector.

Many lenders also controlled costs well. Even as they invested in new systems and security, expense growth stayed manageable. This helped efficiency ratios improve in several cases. As a result, banks entered 2026 with better capital positions and earnings momentum than many had predicted earlier in the year.

Regional Earnings Snapshots

North America: Big U.S. Banks Beat Earnings Expectations

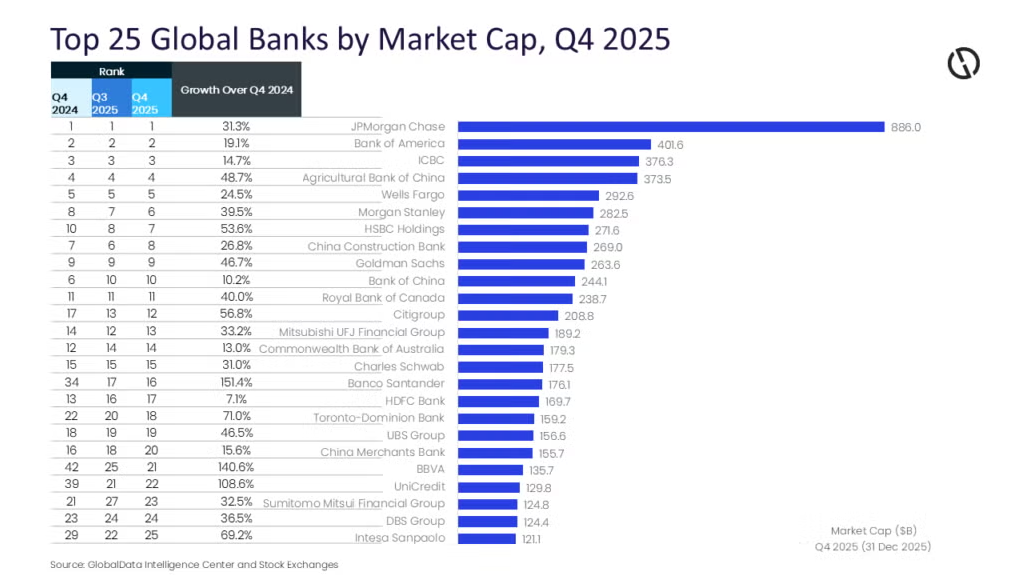

North America saw a strong earnings season to close 2025. Major U.S. banks began reporting in January 2026 with results that beat expectations. JPMorgan Chase posted about $46 billion in revenue, along with strong per-share earnings. Bank of America, Wells Fargo, and Citigroup also reported growth in lending and markets revenue, with loan growth ranging from 5-8% YoY. Strong trading and investment banking activity added to their profits, giving investors confidence as banks enter 2026.

Canada: Stable Q4 Results Support Banking Outlook

Canadian banks ended 2025 with steady earnings. Analysts expected Q4 profits to rise 4-6% YoY, supported by continued loan growth of about 3-5% YoY. Investment banking deals and advisory services also helped revenues, keeping banks profitable despite economic uncertainties. This stability sets a positive stage for Canadian lenders in 2026.

Asia and Africa: Profit Growth Driven by Higher Net Interest Income

Banks in Asia and Africa showed strong growth through mid-2025. Net interest income increased by about 7-9% YoY, while non-interest income rose 5-7% YoY. Loan and deposit portfolios expanded 3-6% YoY, with costs and asset quality well managed. These factors helped many regional banks strengthen their balance sheets and maintain earnings momentum.

Europe: Resilient Bank Earnings Backed by Cost Control

European banks ended 2025 on a resilient note. Loan growth averaged 2-4% YoY, while trading and markets income contributed around 10-12% of total revenue. Improved cost management and efficiency ratios, which rose 1-2% compared to 2024, supported stronger profitability. This solid performance gives European banks confidence as they plan for 2026.

Profitability Drivers Beyond Net Interest Income

Banks no longer rely only on interest margins. Fee income from wealth management, advisory, and trading became vital to earnings in 2025. For example, major U.S. banks posted strong non-interest income growth linked to deal activity and trading. Investment banking fees rebounded as mergers and acquisitions hit multi-trillion-dollar levels, boosting revenue.

Technology also played a role. Banks invested in digital platforms that help lower costs and improve customer experiences. These investments supported fee growth from online services, payments, and digital wallets. Some lenders also increased wealth-management offerings, earning more fees from asset management and investment advice.

However, not all revenue streams grew equally. Some areas, like credit-card fees, faced pressure from policy debates and regulatory proposals that could cap interest rates. These policy talks affected bank stock prices even as earnings remained strong.

Macro & Strategic Trends Shaping 2026

Monetary policy will be crucial in 2026. Many central banks are expected to hold rates steady or cut them gradually. A more stable rate environment could support loan growth and keep net interest margins from shrinking further.

Analysts also point to the role of AI technology in boosting efficiency and creating new revenue channels. Investment in AI helps automate processes, reduce costs, and enhance customer interactions, though these investments can raise short-term expenses.

Strategic mergers in the banking industry continue to reshape the landscape. Recent consolidation deals have expanded scale for some regional banks, creating opportunities for cost savings and broader customer reach.

Geopolitical and economic uncertainty remains a challenge. Fluctuating global growth, trade tensions, and policy changes could affect credit demand and cross-border financing. Banks are watching these risks as they plan growth strategies for 2026.

Risks That Could Temper Growth

Banks face emerging credit risks, especially in consumer and commercial loan portfolios. Analysts expect net charge-offs, the losses from loans that cannot be collected, to rise in 2026, even if they remain moderate. This could put pressure on earnings and require higher reserves.

Interest-rate policy uncertainty also adds risk. If rate cuts are deeper or faster than expected, net interest income could weaken. Similarly, proposals to cap credit card interest rates may reduce profitability for major card issuers.

Another risk is global economic slowing. Some research models suggest a noticeable chance of recession in 2026, which could dampen loan demand and trading activity.

Bank Earnings 2025: What to Watch in 2026?

First, look at early 2026 earnings guidance. Many banks will clarify their expectations for revenue, costs, and loan growth. If loan demand strengthens and costs stay controlled, earnings could expand. Markets will also watch how well banks integrate new technology investments and digital platforms to capture fee income.

Second, strong performers in 2025 may continue to attract investment interest in 2026. Some banks have already shown bullish patterns in stock charts as earnings momentum builds.

Finally, regulatory policy will matter. Any changes in banking rules, consumer protections, or capital requirements could shift earnings outlooks for lenders of all sizes.

Conclusion: Growth Ahead but Not Without Complexity

Bank earnings in 2025 reflected strong performance across lending, trading, and fee income. As we move into 2026, momentum remains but faces headwinds. Stable monetary policy, smart technology investment, and disciplined risk management will be key to sustaining growth. While some risks persist, banks with diversified revenue and solid credit quality are in the best position to thrive in the year ahead.

Frequently Asked Questions (FAQs)

Bank earnings stayed strong due to higher net interest income, stable loan demand, and better fee income from trading and advisory services, according to reports released in December 2025.

Most analysts expect steady bank earnings growth in 2026, supported by stable interest rates, controlled costs, and continued demand for loans, based on outlooks shared in January 2026.

Interest rates influence how much banks earn from loans and deposits. Stable or slow rate cuts in 2026 may support lending but limit further profit margin growth.

Disclaimer

The content shared by Meyka AI PTY LTD is solely for research and informational purposes. Meyka is not a financial advisory service, and the information provided should not be considered investment or trading advice.