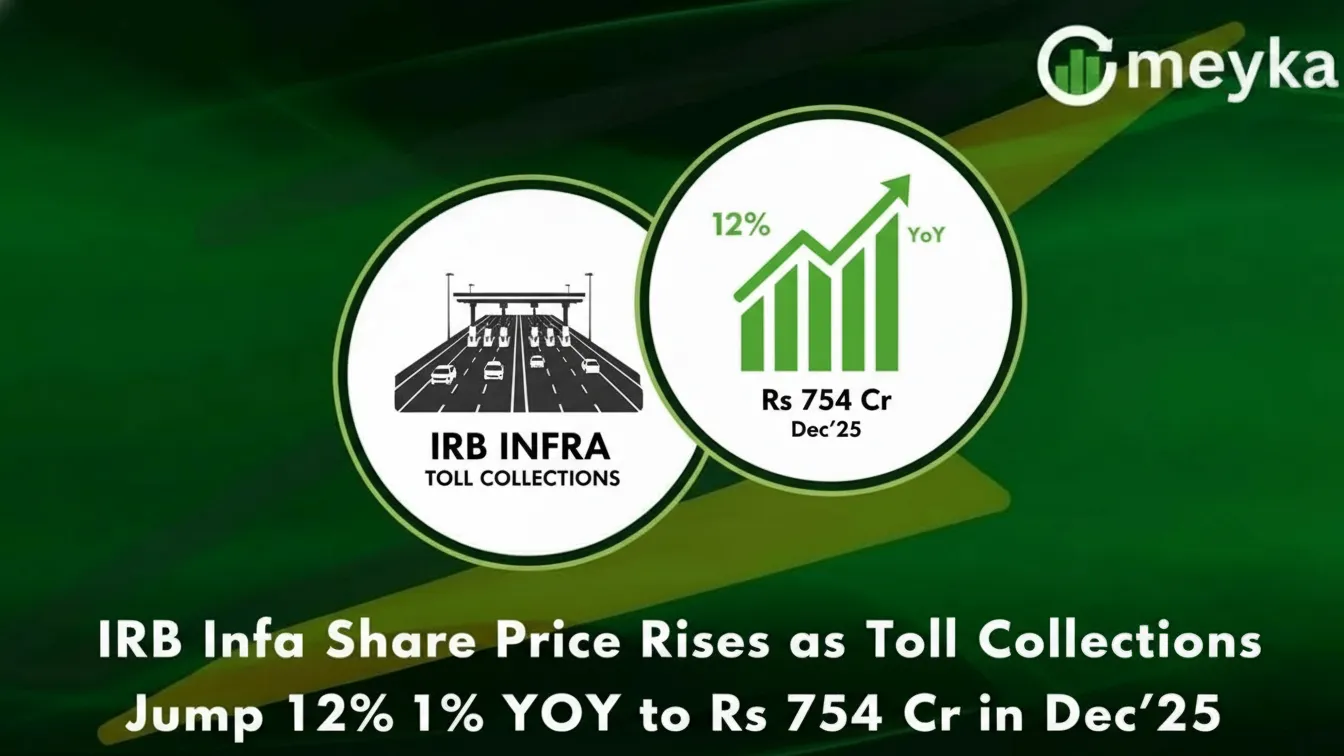

IRB Infra Share Price Rises as Toll Collections Jump 12% YoY to Rs 754 Cr in Dec’25

We begin with some good news for investors watching the IRB Infra share price this week. IRB Infrastructure Developers Ltd reported a strong rise in toll revenue for December 2025. The company’s total toll collections reached Rs 754 crore, up 12% year‑on‑year compared to Rs 675 crore in December 2024. This jump in toll income has boosted market sentiment. Investors reacted positively, and the stock price showed gains on the Indian stock exchanges.

Continue Reading on Meyka

This article is available in full on our main platform. Get access to complete analysis, stock insights, and more.

Read Full Article →